Busting the Trust

An intergenerational saga. Or, when women get sh*t done.

This is the part of the story where three generations of women came together to say:

We are agents of change and our money can be too.

All of us having been told no, you don’t understand or no, this isn’t your decision to make, or no, that doesn’t make sense. By trustees, by men, by our own internal critic.

All of us ready to move beyond the separation of femininity and finance, individual wealth and collective wellbeing, personal prosperity and community care.

And together, we decided to bust some trusts.

I didn’t start out with the intention to bust.

I simply started with the intention to give.

In May of 2021, five months after discovering I had a trust fund worth one million dollars in my name, I wrote to the financial advisors governing this account.

I said: I would like to start exploring ways to redistribute this money. Not necessarily all of it, but some of it — beginning this year with $50,000.

They said (hesitantly): Sure, as long as you don’t give more than $50,000 annually, your investments stay in public markets, and you don’t shrink your portfolio.

I said: Ok.

So I began giving. Mostly to grant making collectives led and governed by people most impacted by extractive capitalism1 (such as Movement 4 Black Lives and NDN Collective), those where decision making power is handed over to the communities receiving the funds.

And here’s what I started to realize:

It felt good to give.

Action in the face of uncertainty and ecological crisis. A way to pair activism with financial resources. Not hide privilege but leverage it. Take my place within a lineage that emphasized caring about others.

So, in July of 2021, when I was made aware of a land rematriation project in my home state of Vermont, I immediately decided to increase my giving — committing an additional $50,000. This totaled $100,000 — 10% of my total assets — for the year.

That month I had also begun digging into the investments in the trust fund and was hit with a sickening hypocrisy:

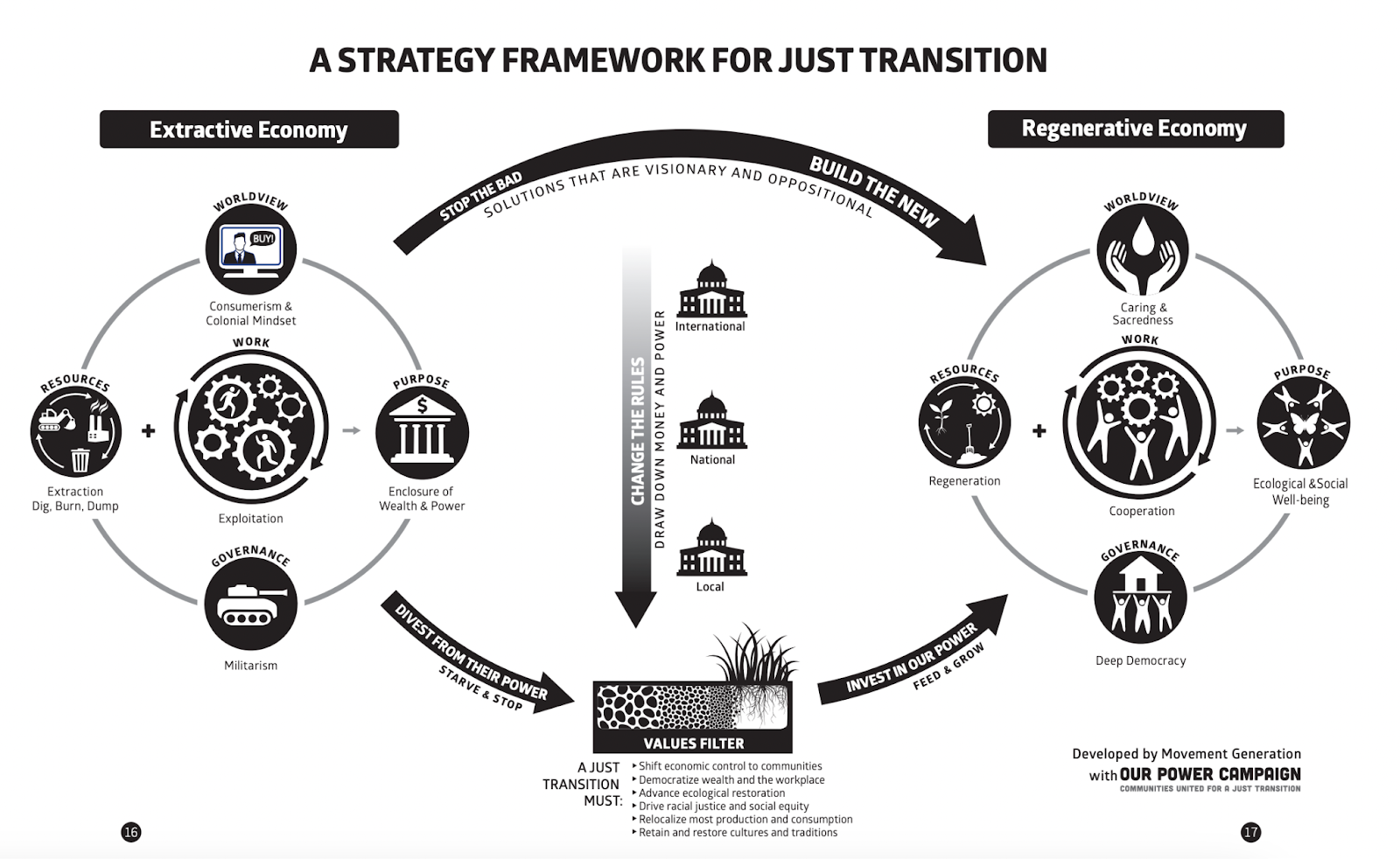

My portfolio, even with ESG screens, centered on publicly-traded multinational corporations. These companies, operating by profit-maximization and cheap labor, reinforce inequitable power structures that exploit people and planet — such as palm oil companies that cut down forests, tech conglomerates that consolidate power in the hands of the few, and private prisons and migrant detention centers that destroy lives and traumatize generations.

Meaning that, at this current ratio, my 4% annual giving attempted to counteract ingrained biases and injustices that I remained 96% invested in.

So, in August 2021,

I said: I would also like to start moving my money out of public markets. Beginning with divesting $250,000 to be reinvested in non-extractive community loan funds.2

But now I had asked to cross all three boundaries:

Give more than $50,000 in one year.

Move investments out of public markets.

(Slightly) Shrink my portfolio.

And here is where the battle began.

Because this is the issue: The wealth management industry is primarily guided by following principles:

Excessive wealth accumulation is completely acceptable if not desirable

Taxation is synonymous with waste2

It is held up by structures, like trust funds, and guarded by people, like my financial advisors, who are trained to protect the wealth at all costs.

The battle scenes:

In September 2021, they said: While the language in your trust allows for flexibility, charitable gifting from a trust, without specific language allowing a trustee to do so, is problematic because of the need to establish the benefit to the beneficiary (me).

I said: This work benefits all of us, not just those directly receiving funds. It centers those who are most impacted by systemic inequity as key decision-makers, and respects their self-determination, while ultimately creating conditions that will promote health, safety, and happiness for everyone (for example, solutions to climate change). I know that this is pivotal to my own future, as well as the future of my own potential family, and as such a “benefit to the beneficiary.”

They said: But the trust is not an outright gift. In our role we must honor what the trust was set up to do which was by your grandfather to provide for his grandchildren over the course of the rest of our lives, and that is separate from charity.*

Which translates to the system, wealth management/defense, saying: We will support individual wealth accumulation, but not anything that threatens money moving outside of the bloodline.

*Disclaimer

Use of the word charity.

Charity has long created separation between those who give and those who receive. This has been the foundation of a philanthropic culture in which you must accumulate in order to be generous.

There must be an underlying shift in the way philanthropy is approached, moving from a model based in charity — that “which perpetuates power dynamics between givers and receivers without tackling root causes of injustice” — to one of regeneration — “based on reflective, responsive, reciprocal relationships of interdependence between human communities and the living world” (“From Banks to Tanks” 2017).

Another way to frame this: Moving from charity to solidarity.

When it came to investment:

They said (of Seed Commons, my proposed community loan fund): These are below market rate returns. Our primary responsibility is to take care of your personal financial needs so we need to understand what made you want to do impact investing? What is your overall goal, and what are you trying to achieve?

I said: To be “invested” in something is to care about its outcome and to understand our interconnectedness.3 I have no interest in corporations that compromise our future resources to secure personal profit. I believe this to be inhibiting the future safety of myself, my family, and my communities more broadly.

Those of us with power in capital markets can shift some of that power and reframe investing to create powerful societal transformation. I am in the position to catalyze funds that are looking to do just that, and want to leverage the money I have inherited beyond individual and into collective benefit.

In October 2021, they said: We have been struggling with your requests because, while admirable, it is our responsibility (acting on behalf of a structure) to ensure that the trust be used over the course the rest of your life, as your grandfather intended (which, to be clear, was never cited). This means ultimately the level of giving and divestment you propose is not within your jurisdiction and therefore we will be divesting no more than $100k and limit your giving no more than 3-4% annually.

I said: Will you reconsider?

And they said: No.

Which translates to the system, wealth management/defense, saying:

Financial return on your behalf takes precedence over other kinds of return (return to community, to those whose lands and labor was extracted from; return to the planet and practices that put us back in balance with her).

Also, we, the structure, risk losing income if you shrink your assets. This business model is one based in constant, unquestioned growth.

Here is where the family re-enters. The generations of women.

My mom — who had taken her own risks to build a life in a small town, own a small business, build community across class, and create meaningful change in local geographies. Who had shown up to every call, who had listened to me process the feelings of guilt and shame, even when panicking that her child was trying to give away an entire safety net. Who engaged with debate rather than patronization, and curiosity rather than defensiveness.

My grandmother — who traveled the country and the world looking for and supporting activists fighting to preserve and save the landscapes she saw eroding. Who had felt her own desire to give back to community suppressed by financial structures and who didn’t hesitate when I asked for her help.

Both of them understood money to be a tool for change and expression of values. A way to walk the talk. To do something, rather than nothing.

And now the motivation had shifted: from simply wanting to give and invest in alignment with my values, to having the agency to make decisions over resources left in my name.

So, in October 2022, we— mother/daughter/granddaughter — said: We would like to see the trust documents to understand exactly what our rights are.

And in November 2022, we — mother/daughter — said: We would like to shift trustees.

To which, the trust structure said: No, it within our jurisdiction to make decisions for you that maintain your financial interest.

So we,— mother/daughter/granddaughter — said: Our interest goes beyond financial. Who are the people that can speak to the structure and be taken seriously within the system?

Enter the lawyer. Let’s call him Ike.

An attorney in his late 70s, Ike had helped my grandfather set up these trust funds in the first place. And he agreed to get on a call.

In November 2023, on a call with Ike, we said: We want to be able to activate an entire portfolio beyond just what was allocated to “philanthropy” — to have our investments mirror our giving and not counteract it. In this trust structure we are trapped in investments we don’t believe in, and we want out.

He said (and this was and maybe still is the biggest surprise of them all):

That doesn’t seem at all crazy. Let’s remove that trust company as your trustee!

So with Ike’s support and legal translation, we made our final case to the trust company.

We did it with deep love and pride in our family, in our lineage, and the platform and resources it gave us to push for meaningful change in a society that is not fit to sustain anyone, regardless their level of wealth. And with that recognition of responsibility, and (crucially), support across generations,

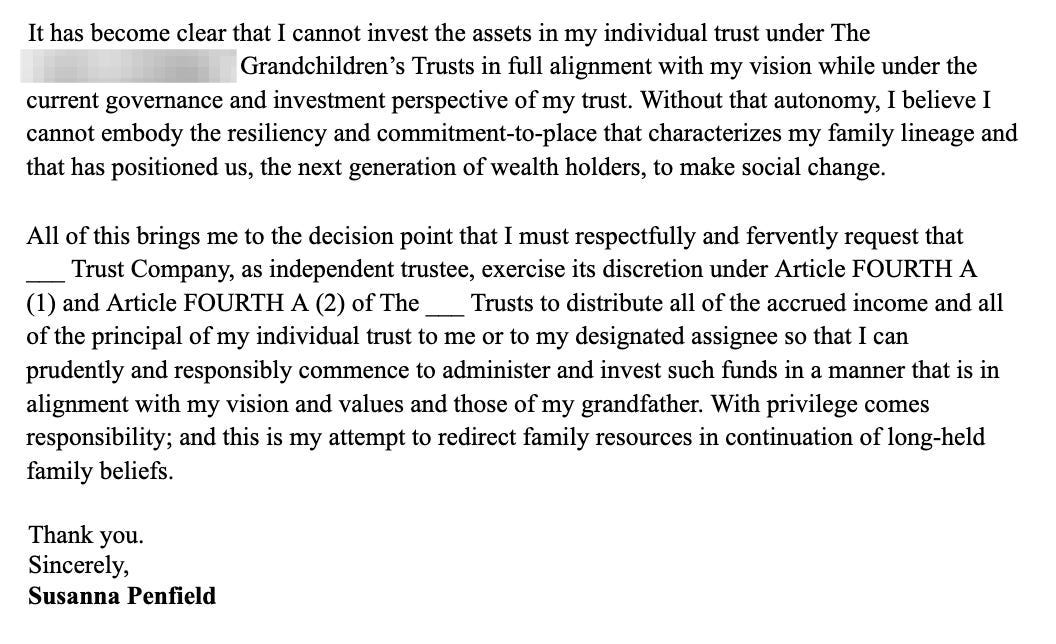

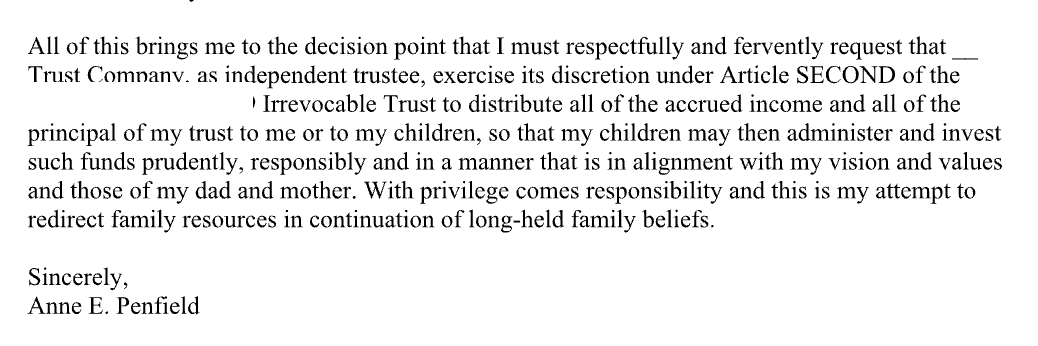

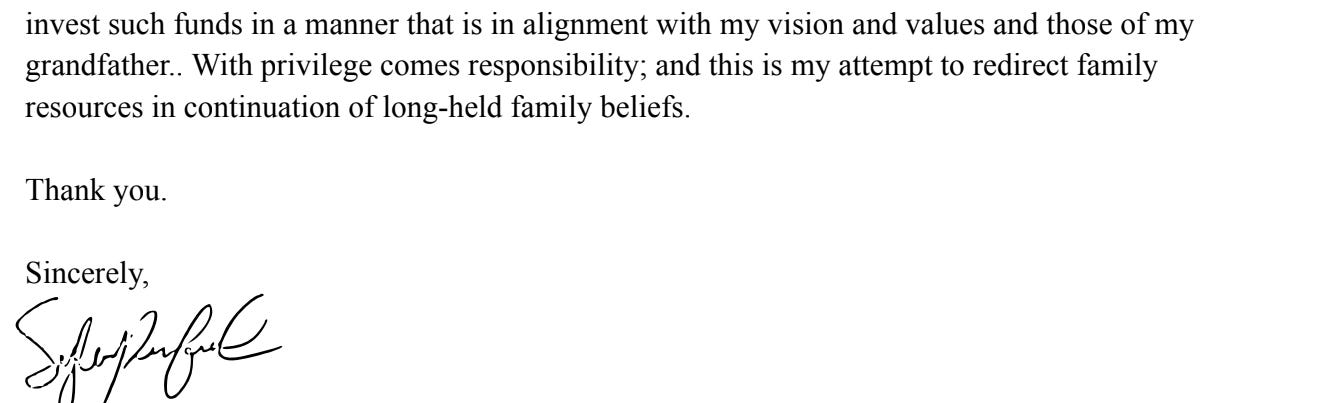

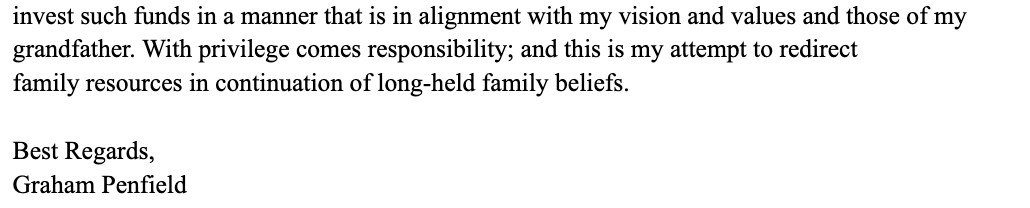

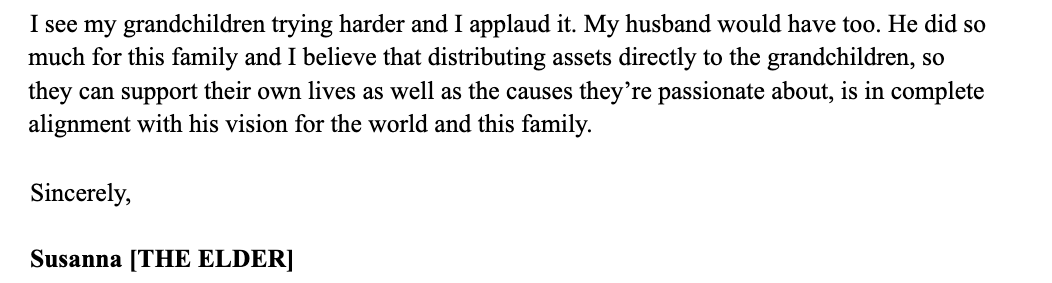

December 2023, I wrote:

And my mom wrote:

And my sister wrote (yay siblings!):

And my brother wrote (not just the women!):

And my grandmother wrote (and this really sealed the deal):

And in January 2024, they (finally) said: Ok. Enough. We are prepared to outright distribute all assets to you.

To which we said: Trust, BUSTED?!

And Ike said:

Which is how we found ourselves liberated from a structure and given options for how to navigate a system. And isn’t that all anyone deserves? Agency over their own resources? To give, invest, and live with integrity?

Remember, hard on structure, soft on people.

I mean this in terms of both the people who represent the structures (the financial advisors, trustees, attorneys) as well as the people who inherit the structures.

It took 4 years for me, a person with education, class privilege and eldest-daughter persistence, to move from a simple question — What can I do with this money so that it makes a positive (even if minor) difference in the world? — to actually unlock the resources that could allow me to do so. And this was with family support, community encouragement (Resource Generation, Just Economy Institute), the time to commit, and fortuitous connections (Ike!). Things many people don’t have.

These structures are meant to grow wealth above all else, often in perpetuity, and often against any intent expressed by those whose names are on them.4 All while we are living in a time where wealth inequity is quite possibly the most extreme it has ever been.

Which is why we need more examples of people willing to challenge these structures. Stories of those who have found (and forged) pathways to liberate these resources. And that’s exactly where this series is planning to go.

Coming next: The Other Trust-Busters (spoiler alert: it’s not just me).

Social Justice Giving Principles, Resource Generation.

Seed Commons! Check them out and other alternative funds here: Transformative 25.

Transformative Investment Principles, Resource Generation.

For more on the structures, read Offshore: Stealth, Wealth and the New Colonialism by Brooke Harrington.

Love this! And want to sing along to the Ghostbusters soundtrack, "Who you gonna call? Trust Busters!" 👻 📜🛠️⛓️💥

Love reading this - the outcomes, the journey, the candor in the various roles....thank you for sharing!